In personal finance, two products often come up in discussions about financial security and wealth building—Life Insurance and Investment Plans. While both play crucial roles, their purposes, benefits, and risks differ significantly.

Many people confuse the two, assuming life insurance is a type of investment or that investment plans can replace life insurance. In reality, they serve complementary but distinct financial needs.

In this detailed guide, we’ll break down the differences, pros, cons, costs, and strategies of life insurance vs investment plans so you can make informed financial decisions.

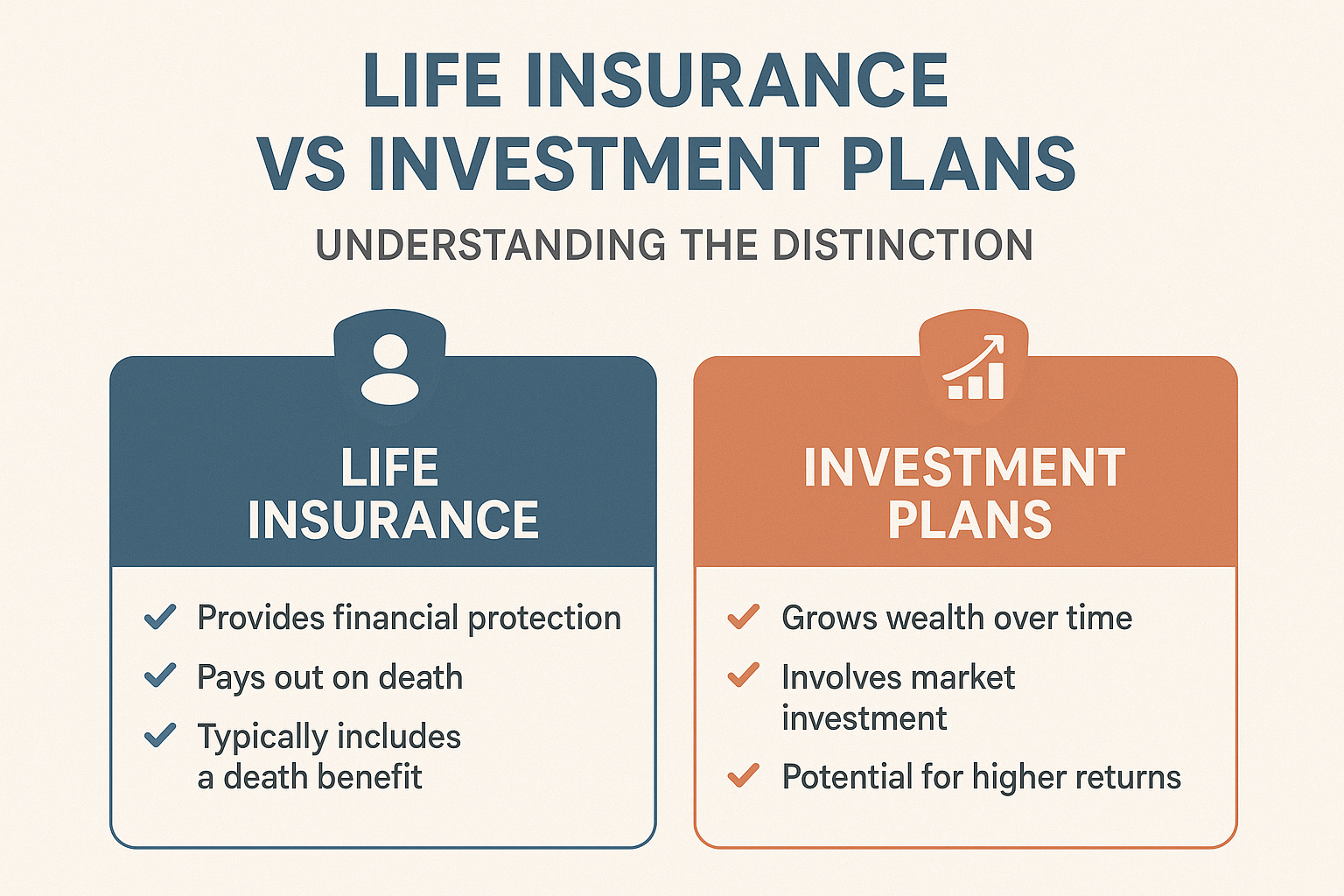

What Is Life Insurance?

Life insurance is primarily a risk management tool designed to provide financial protection to your loved ones in case of your untimely death.

When you purchase a life insurance policy, you pay regular premiums, and in return, your beneficiaries receive a death benefit payout if you pass away during the policy term.

Types of Life Insurance:

- Term Life Insurance – Pure protection plan with no savings component; most affordable.

- Whole Life Insurance – Lifetime coverage with a cash value component.

- Universal Life Insurance – Flexible premiums and coverage with an investment portion.

- Endowment Plans – Combines insurance with savings, paying a lump sum at maturity.

What Are Investment Plans?

Investment plans are financial products designed to help you grow wealth by putting money into different assets. Unlike life insurance, their core purpose is wealth accumulation and financial growth.

Common Types of Investment Plans:

- Stocks and Equity Mutual Funds – High growth potential, higher risk.

- Bonds and Fixed Deposits – Stable but lower returns.

- Retirement Plans / 401(k) / Pension Funds – Long-term wealth for retirement.

- Unit Linked Insurance Plans (ULIPs) – Hybrid plans combining insurance and investment.

- Real Estate Investments – Tangible asset-based wealth creation.

Key Differences: Life Insurance vs Investment Plans

| Feature | Life Insurance | Investment Plans |

|---|---|---|

| Primary Purpose | Financial protection for dependents | Wealth creation and financial growth |

| Payout | Death benefit to nominee (or maturity benefit in some) | Returns depend on market performance or interest |

| Risk Level | Low (guaranteed payout in case of death) | Varies (low for bonds, high for equities) |

| Tax Benefits | Premiums often tax-deductible under Sec 80C/80D | Investment gains may have capital gains tax |

| Liquidity | Limited (except for cash value policies) | Higher liquidity (stocks, mutual funds, etc.) |

| Best For | Family protection, income replacement | Wealth building, long-term financial goals |

Why Choose Life Insurance?

Life insurance ensures financial stability for your family if something happens to you.

Benefits:

- Provides peace of mind knowing your dependents are secure.

- Covers loans, mortgages, and daily expenses for your family.

- Affordable premiums, especially for term life insurance.

- Tax benefits under Section 80C and Section 10(10D) in many countries.

Example Scenario:

Rahul, 35, earns $60,000 annually and has two children. By purchasing a $500,000 term life policy, his family is financially secure for years in case of his death.

Why Choose Investment Plans?

Investment plans are best for wealth creation and achieving financial goals like retirement, children’s education, or buying a home.

Benefits:

- Potential for high returns through equity markets.

- Helps combat inflation with long-term growth.

- Offers flexibility in investment options (stocks, bonds, mutual funds).

- Builds retirement wealth and passive income streams.

Example Scenario:

Aditi, 30, invests $500 monthly in a diversified mutual fund. Over 20 years, assuming 10% annual returns, she grows her investment to over $300,000, securing her retirement.

Life Insurance vs Investment: Common Misconceptions

- “Life insurance is an investment.”

- Term life is purely protection, not an investment. Only ULIPs or endowment policies combine both.

- “Investments can replace life insurance.”

- Investments grow wealth, but they don’t guarantee financial security for dependents in case of death.

- “Life insurance is a waste if I don’t die early.”

- Life insurance is like a safety net—its value lies in protecting your family against uncertainty.

Cost Comparison: Life Insurance vs Investment

- Life Insurance (Term Plan):

- Very affordable—$20–$30/month can secure $500,000 coverage.

- Investment Plans:

- Varies widely—$100 to thousands monthly, depending on asset type and goals.

👉 Insurance protects your family’s present security, while investments build your future wealth.

Can You Combine Life Insurance and Investment?

Yes! A smart financial strategy often includes both insurance and investments.

Options:

- Buy a Term Life Insurance policy for protection.

- Invest separately in mutual funds, ETFs, or retirement accounts for wealth growth.

- Avoid mixing the two (like ULIPs) unless you specifically want hybrid plans.

This “buy term, invest the rest” approach ensures maximum coverage at minimal cost while still building wealth.

Pros and Cons

Life Insurance

Pros:

- ✔ Affordable premiums

- ✔ Provides family security

- ✔ Tax benefits

- ✔ Fixed, predictable payout

Cons:

- ✘ No wealth growth (in pure term plans)

- ✘ Limited liquidity

Investment Plans

Pros:

- ✔ Higher returns potential

- ✔ Flexible options (equity, bonds, real estate)

- ✔ Helps beat inflation

- ✔ Builds long-term wealth

Cons:

- ✘ Higher risk

- ✘ Market fluctuations can affect returns

- ✘ No death benefit protection (unless combined with insurance)

Who Should Prioritize Which?

- Choose Life Insurance if:

- You are the primary earner with dependents.

- You have debts like mortgages or loans.

- You want to ensure financial protection for your family.

- Choose Investment Plans if:

- You want to build wealth for long-term goals.

- You have disposable income beyond essential expenses.

- You are saving for retirement, education, or major life milestones.

Real-Life Case Studies

- Life Insurance Example:

Arjun, a young professional, dies in an accident. His $750,000 term life insurance policy allows his wife and children to pay off debts, cover living costs, and continue education.

- Investment Plan Example:

Sneha invests $1,000/month in index funds. Over 25 years, her portfolio grows to $1 million, funding her retirement lifestyle.

Expert Financial Tips

- Always secure life insurance first before focusing on investments—protection comes before growth.

- Choose term insurance over endowment/ULIP if cost efficiency is your priority.

- Diversify investments across stocks, bonds, and retirement accounts.

- Review policies annually to adjust coverage and investments.

- Don’t overpay for hybrid products unless they suit your unique goals.

Conclusion: Life Insurance vs Investment Plans

Both life insurance and investment plans are essential tools, but they serve different purposes.

- Life Insurance → Provides financial protection for dependents.

- Investment Plans → Focus on wealth creation and financial growth.

👉 The best financial strategy isn’t choosing one over the other but balancing both. Secure your family with affordable term life insurance and grow wealth with smart investments.

By understanding the clear distinction between the two, you can create a comprehensive financial plan that ensures both security and prosperity.