In today’s uncertain world, protecting your health and financial future is more important than ever. While most people focus on health insurance or life insurance, they often overlook two critical types of coverage: Critical Illness Insurance and Disability Insurance.

At first glance, these policies may seem similar—they both provide financial protection when health issues impact your ability to earn. However, the way they work, what they cover, and how they pay benefits are very different.

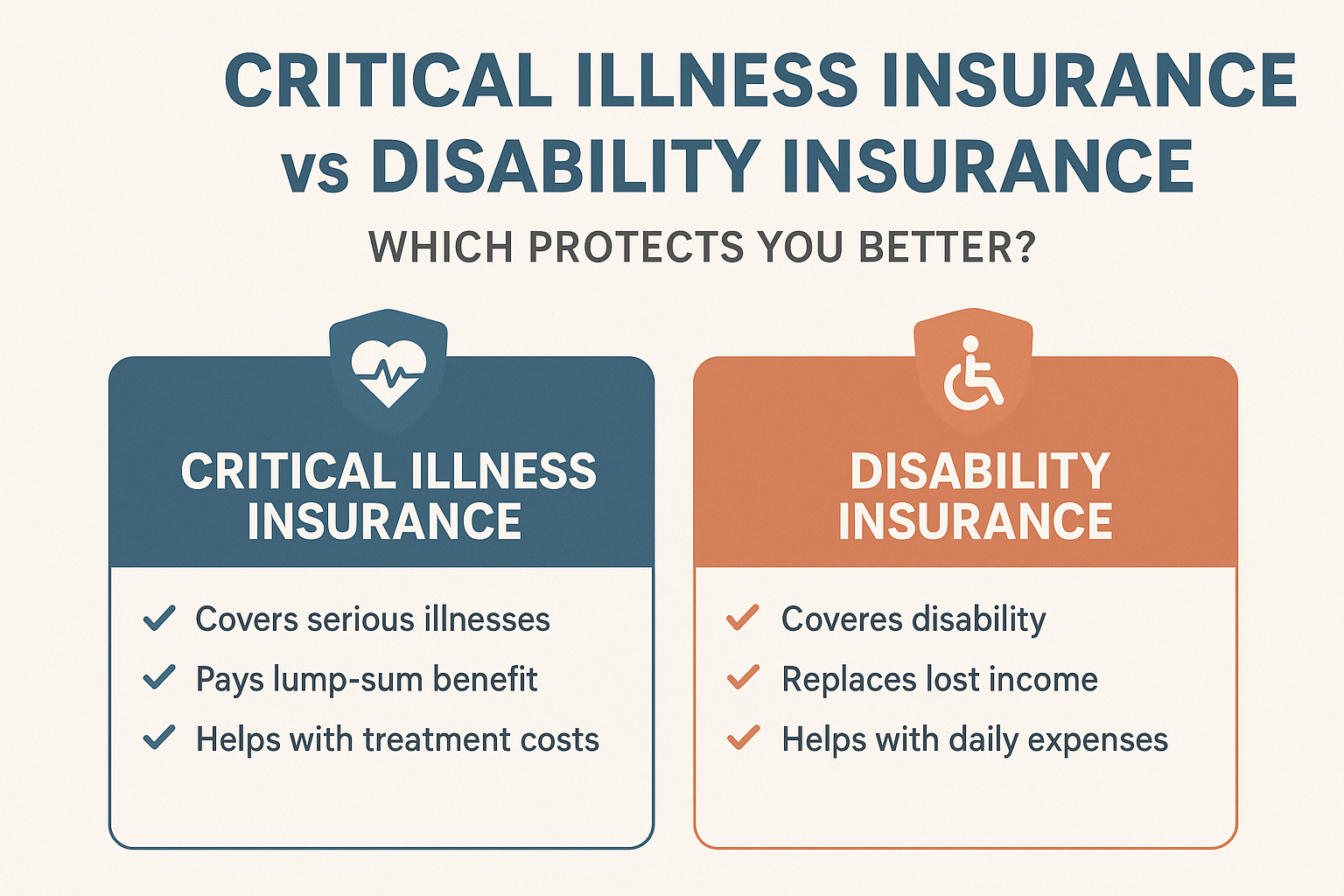

In this guide, we’ll break down the key differences, benefits, costs, and real-life scenarios to help you decide which type of insurance—critical illness insurance or disability insurance—is right for you.

What Is Critical Illness Insurance?

Critical illness insurance provides a lump-sum payout if you are diagnosed with a covered serious illness. This one-time payment can be used however you choose—medical bills, mortgage payments, or even experimental treatments not covered by your health plan.

Common Illnesses Covered:

- Cancer

- Heart attack

- Stroke

- Kidney failure

- Organ transplant

- Multiple sclerosis

- Paralysis

Key Features of Critical Illness Insurance:

- Lump-sum payment upon diagnosis

- Can be used for medical or non-medical expenses

- Often comes with fixed coverage amounts (e.g., $25,000 – $100,000)

- May have waiting periods and exclusions for pre-existing conditions

What Is Disability Insurance?

Disability insurance provides ongoing income replacement if you become unable to work due to illness or injury. Instead of a lump sum, you receive monthly benefits that replace a percentage of your lost income.

Types of Disability Insurance:

- Short-Term Disability (STD): Covers temporary disabilities for a few months.

- Long-Term Disability (LTD): Provides benefits for years—or even until retirement—if you can’t work.

Key Features of Disability Insurance:

- Monthly income replacement (50–70% of salary)

- Covers both illnesses and injuries

- Benefits continue as long as you’re disabled (based on policy)

- Premiums depend on age, occupation, and coverage level

Why Choose Critical Illness Insurance?

Critical illness insurance is best for those worried about serious health diagnoses that come with high medical costs.

Example Scenarios:

- You’re diagnosed with cancer and need chemotherapy → Insurance pays a lump sum to cover treatment and living expenses.

- You have a heart attack and need months of recovery → The payout helps pay your mortgage, childcare, or debts.

👉 Critical illness insurance works as a financial cushion when facing life-threatening conditions.

Why Choose Disability Insurance?

Disability insurance is essential for protecting your income stream when you can’t work.

Example Scenarios:

- You suffer a back injury in a car accident and can’t work for a year → Disability insurance replaces 60% of your salary.

- You develop a chronic illness like multiple sclerosis that limits your ability to work long-term → Long-term disability benefits cover your ongoing income needs.

👉 Disability insurance is best if your salary is your primary financial asset.

Cost Comparison: Critical Illness vs Disability Insurance

- Critical Illness Insurance Premiums:

- $15–$50 per month (depending on age and coverage amount).

- Lower cost because it only covers specific illnesses.

- Disability Insurance Premiums:

- 1–3% of your annual salary.

- More expensive, but provides comprehensive income protection.

Can You Have Both Policies?

Yes—and in many cases, it makes sense to carry both critical illness and disability insurance.

- Critical Illness Insurance → Helps cover immediate, high medical bills and one-time costs.

- Disability Insurance → Ensures steady income if you can’t work for months or years.

Together, they provide comprehensive financial protection against unexpected health crises.

Pros and Cons

Critical Illness Insurance

Pros:

- ✔ Lump-sum payout you can use freely

- ✔ More affordable premiums

- ✔ Helps with out-of-pocket medical costs

Cons:

- ✘ Only covers specific illnesses

- ✘ No ongoing income replacement

- ✘ Limited payout amounts

Disability Insurance

Pros:

- ✔ Provides regular income replacement

- ✔ Covers both illnesses and accidents

- ✔ Long-term financial security

Cons:

- ✘ Higher premiums

- ✘ More complicated underwriting

- ✘ Waiting periods before benefits begin

Who Needs Which Type of Insurance?

- Critical Illness Insurance is best for:

- Individuals with family health histories of cancer, heart disease, or stroke

- People without strong emergency savings

- Those seeking an affordable way to supplement health coverage

- Disability Insurance is best for:

- High-income professionals (doctors, lawyers, engineers, etc.)

- Sole breadwinners in families

- Self-employed individuals without employer coverage

Real-Life Case Studies

- Critical Illness Example:

- Maria, 42, was diagnosed with breast cancer. Her critical illness policy paid $50,000, which she used for treatment costs and mortgage payments while she focused on recovery.

- Disability Insurance Example:

- David, 35, a software engineer, suffered a spinal injury in a car crash. His long-term disability policy replaced 65% of his income for two years while he underwent rehabilitation.

Expert Tips for Choosing the Right Policy

- Evaluate Your Income Dependence – If your family relies heavily on your salary, disability insurance is essential.

- Consider Family Medical History – If you have a high risk of critical illnesses, a lump-sum policy is worth it.

- Combine Policies if Possible – For complete protection, pair both coverages.

- Compare Multiple Providers – Always shop around for the best insurance quotes.

- Check Exclusions and Waiting Periods – Understand when coverage begins and what’s not included.

Conclusion: Critical Illness vs Disability Insurance

Both critical illness insurance and disability insurance serve unique, valuable roles in financial protection.

- Critical Illness Insurance → Best for covering large, sudden expenses from major health diagnoses.

- Disability Insurance → Best for ensuring a steady income when illness or injury prevents you from working.

👉 The smartest choice? Consider combining both policies. This way, you’ll have a safety net for both one-time medical expenses and long-term income replacement.