When planning a trip, most people think of booking flights, packing bags, and creating itineraries. But one critical element often overlooked is insurance coverage. Many travelers are confused about whether they need travel insurance, health insurance, or both. While the two types of insurance may seem similar, they serve very different purposes.

Understanding the difference between travel insurance and health insurance can save you from unexpected medical bills, canceled trip costs, or even financial disaster abroad. This guide will explain the key differences, benefits, costs, and real-world scenarios so you can make an informed decision.

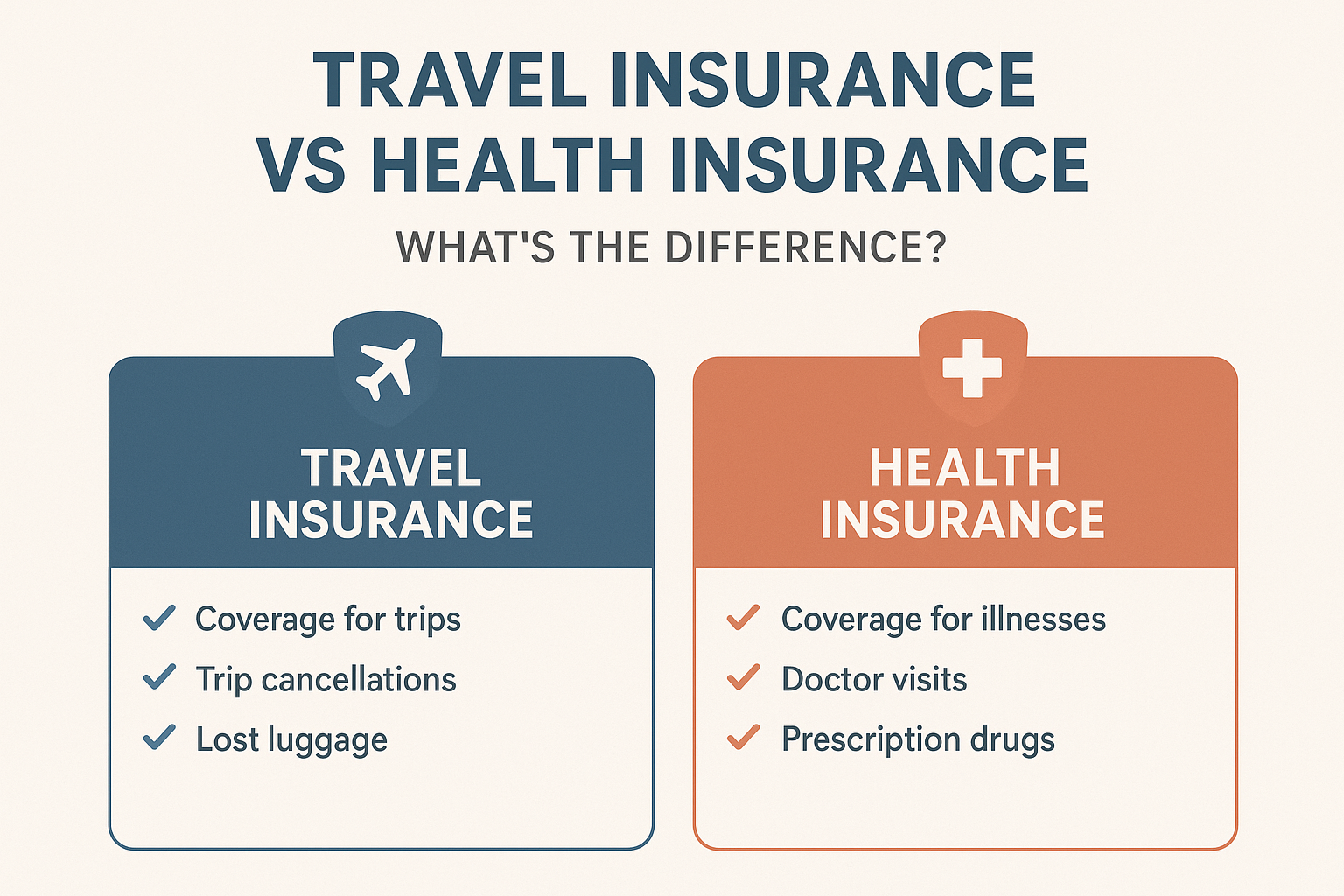

What Is Travel Insurance?

Travel insurance is designed to protect you financially from unexpected problems during a trip—whether domestic or international. It typically covers:

- Trip Cancellation or Interruption – Reimbursement for prepaid travel expenses if your trip is canceled or cut short due to illness, family emergencies, or natural disasters.

- Emergency Medical Coverage Abroad – Pays for medical treatment if you get sick or injured while traveling internationally.

- Lost Baggage and Delays – Compensation for lost, stolen, or delayed luggage.

- Travel Accident Insurance – Provides compensation in case of accidental death or disability while traveling.

- 24/7 Travel Assistance Services – Helps with rebooking flights, locating hospitals, or arranging emergency evacuations.

What Is Health Insurance?

Health insurance is a long-term coverage plan that helps pay for medical expenses like doctor visits, hospital stays, surgeries, and prescription drugs. It is not designed for short-term travel but rather for your everyday healthcare needs.

Typical Health Insurance Coverage:

- Doctor Visits & Consultations

- Hospitalization & Surgery

- Prescription Drugs

- Preventive Care (vaccines, check-ups, screenings)

- Maternity & Mental Health Services

- Specialist Care (dentists, dermatologists, etc.)

Travel Insurance vs Health Insurance: Key Differences

| Feature | Travel Insurance | Health Insurance |

|---|---|---|

| Purpose | Short-term protection for trips | Long-term healthcare coverage |

| Coverage Duration | Specific to trip dates (e.g., 1 week to 6 months) | Ongoing (annual or multi-year policies) |

| Medical Coverage | Only during travel, often limited | Comprehensive coverage within your country |

| Emergency Evacuation | Included in many plans | Rarely included |

| Prescription Drugs | Usually not covered unless emergency | Regular coverage |

| Cost | $30–$200 per trip (average) | $3,000–$8,000 per year (U.S. average) |

| Legal Requirement | Not mandatory but recommended | Often mandatory (employer or government plans) |

Why Travel Insurance Matters

Travel is unpredictable—flights get canceled, bags go missing, and medical emergencies can happen without warning. Travel insurance ensures that you don’t pay out of pocket for these surprises.

Example Scenarios:

- You develop appendicitis in Thailand and need surgery → Travel insurance pays for hospitalization.

- Your flight is canceled due to bad weather → Trip cancellation coverage reimburses your hotel and ticket costs.

- Your luggage with valuables is lost by an airline → Travel insurance compensates you for the loss.

Why Health Insurance Matters

Health insurance provides ongoing protection against the high cost of medical care. Without it, even basic healthcare can drain your finances.

Example Scenarios:

- You need routine blood tests or annual check-ups → Health insurance covers preventive care.

- You’re diagnosed with a chronic illness like diabetes → Health insurance helps cover long-term treatment costs.

- You require emergency surgery at home → Health insurance ensures you don’t face medical bankruptcy.

Can Travel Insurance Replace Health Insurance?

No. Travel insurance is temporary and limited. It only covers emergencies while you’re abroad. Once you return home, you still need health insurance for ongoing care.

👉 For example, travel insurance might cover an emergency surgery abroad but will not pay for long-term rehabilitation or follow-up care once you’re back in your country.

Can Health Insurance Replace Travel Insurance?

Not really. Most domestic health insurance plans do not cover international travel. Even if they do, coverage is limited and does not include benefits like trip cancellation, lost luggage, or emergency evacuation.

👉 Example: If you break your leg in Europe, your U.S. health insurance might not cover the medical expenses. Without travel medical insurance, you could face bills in the tens of thousands of dollars.

Cost Comparison: Travel Insurance vs Health Insurance

Travel Insurance Costs:

- Short trips → $30–$50 per trip.

- Longer trips (3–6 months) → $100–$500.

- Premium international plans with medical evacuation → $500–$1,000.

Health Insurance Costs:

- U.S. Average: $3,000–$8,000 annually (per person).

- Employer-Sponsored Plans: Lower cost due to contributions.

- Private Health Insurance: Higher premiums but more flexibility.

Additional Coverage Options

Travel Insurance Add-ons:

- Adventure Sports Coverage (skiing, scuba diving, etc.)

- Rental Car Protection

- Cancel for Any Reason (CFAR) Insurance

- Baggage Delay Benefits

Health Insurance Add-ons:

- Dental & Vision Coverage

- Maternity Coverage

- Critical Illness Riders

- Long-term Disability Insurance

Which One Do You Need?

The right choice depends on your situation:

- If you’re traveling abroad → Get travel insurance with medical coverage.

- If you live and work in one country → Health insurance is non-negotiable.

- If you’re an expat or long-term traveler → You may need both travel and international health insurance.

Real-Life Case Studies

- Travel Insurance Example: Emma was on a 2-week trip to Spain when she slipped and fractured her ankle. Her travel insurance covered hospital bills and extended stay expenses.

- Health Insurance Example: John, a U.S. citizen, was diagnosed with cancer. His comprehensive health insurance covered surgery, chemotherapy, and prescription drugs, saving him from financial ruin.

Pros and Cons: Travel vs Health Insurance

Travel Insurance Pros

- ✔ Affordable for short trips

- ✔ Covers medical emergencies abroad

- ✔ Includes trip cancellation, baggage loss, and delays

Travel Insurance Cons

- ✘ Limited medical coverage

- ✘ Not valid for long-term healthcare

- ✘ Only covers you during trip duration

Health Insurance Pros

- ✔ Comprehensive and ongoing coverage

- ✔ Covers preventive and chronic care

- ✔ Essential for financial security at home

Health Insurance Cons

- ✘ More expensive than travel insurance

- ✘ May not cover international travel

- ✘ Complex policies with exclusions

Tips for Choosing the Right Policy

- Compare Multiple Providers – Use comparison websites for health and travel insurance quotes.

- Check Coverage Limits – Look for high medical coverage (at least $100,000 for travel insurance).

- Look for Exclusions – Many policies exclude pre-existing conditions.

- Consider Bundled Plans – Some companies offer combined travel + health coverage for expats.

- Read Reviews of Insurance Providers – Choose from the best insurance companies with a strong claim settlement record.

Conclusion: Travel Insurance vs Health Insurance

Both travel insurance and health insurance are essential, but they serve different purposes:

- Travel Insurance → Protects you during trips with emergency medical coverage, cancellations, and baggage protection.

- Health Insurance → Provides comprehensive, long-term healthcare protection for everyday life.

👉 The best approach? Have both. Use health insurance for routine and long-term care, and travel insurance for emergencies and unexpected events abroad.